C&I Energy Storage Is Exploding Worldwide: Why 500kW–2MWh Systems Are Becoming the New Standard

Fun Facts of BESS

C&I energy storage is no longer a niche — it's becoming the backbone of global industrial power.

Why are 500kW–2MWh systems exploding in popularity across factories, logistics parks, and commercial facilities worldwide?

Over the past decade, energy storage has been dominated by utility-scale mega-projects—large 50–200 MW plants designed to stabilize national grids. But in 2024–2025, a different segment is quietly stealing the spotlight: Commercial & Industrial (C&I) energy storage, particularly systems in the range of 500 kW to 2 MWh.

From factories in South Africa to cold-storage facilities in Southeast Asia and logistics parks in Europe, this size band has suddenly become the “sweet spot” of the global market. And the reasons behind this shift reveal a major structural change in how businesses think about electricity.

1. Electricity prices are more volatile than ever

Across most regions, industrial customers are exposed to increasingly unpredictable electricity costs. Key drivers include:

Post-pandemic grid stress

Fuel price volatility

Growth of intermittent renewables

Transmission bottlenecks

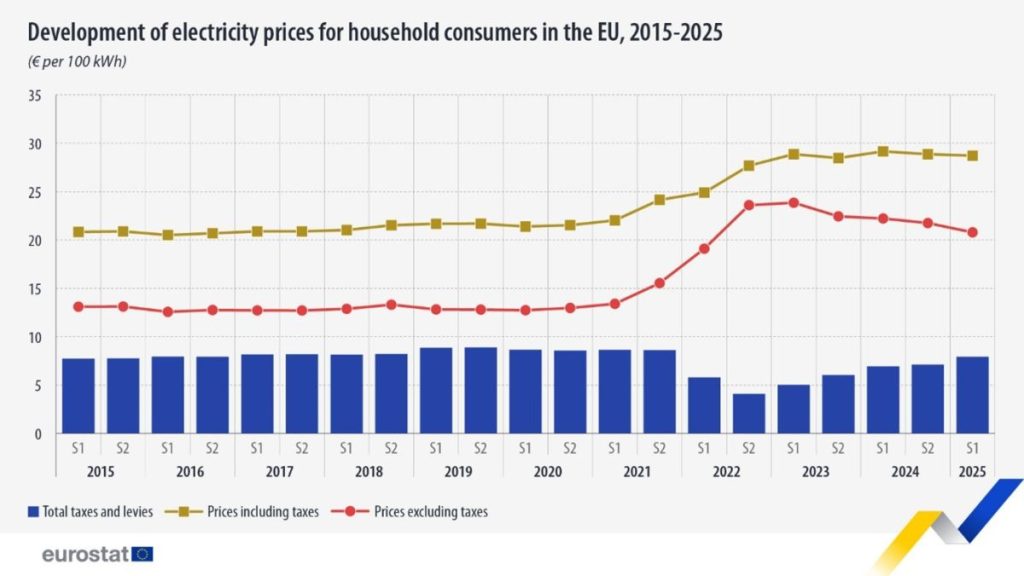

In Europe, industrial electricity prices more than doubled between 2021 and 2023, according to Eurostat.

In the U.S., peak vs. off-peak tariffs continue to widen, with demand charges contributing up to 50% of monthly bills (U.S. EIA).

And in emerging markets such as South Africa, the Philippines, and Pakistan, frequent grid outages amplify the problem—businesses aren't just paying more, the're losing productivity.

A 500 kW–2 MWh system is large enough to shave peak loads AND provide backup power, without requiring the capital intensity of a utility-scale plant.

2. Energy storage is finally affordable

Battery prices have fallen more than 80% in the past decade. BloombergNEF reports that LFP pack prices are approaching $100/kWh in 2024–2025:

This single trend makes C&I storage economically viable for the first time.

At today's prices:

A 1 MWh system can achieve payback in 2.5–4 years in Europe

500 kW systems often see ROI in 2–3 years in Southeast Asia

Markets with diesel backup (Africa, islands) see even faster returns

When a technology crosses the “economic tipping point,” adoption accelerates exponentially—and that is exactly what is happening now.

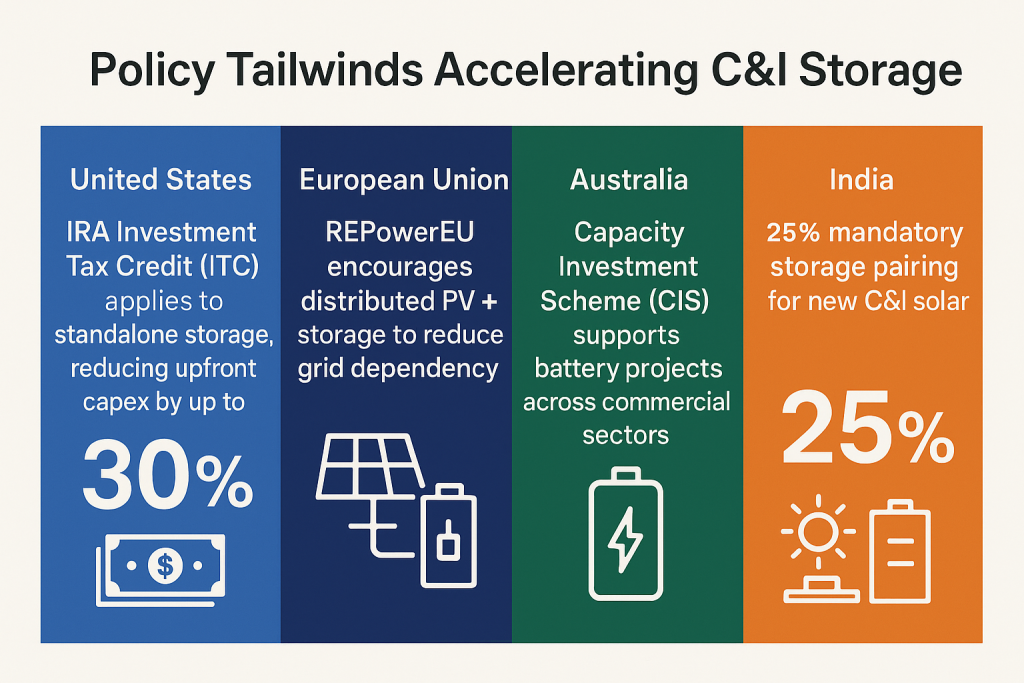

3. Policy tailwinds are pushing C&I projects forward

While utility-scale incentives get most of the headlines, many governments are quietly shaping policies that favor mid-scale C&I deployments.

Examples include:

United States – IRA Investment Tax Credit (ITC) applies to standalone storage, reducing upfront capex by up to 30%

European Union – REPowerEU encourages distributed PV + storage to reduce grid dependency

Australia – Capacity Investment Scheme (CIS) supports battery projects across commercial sectors

India – 25% mandatory storage pairing for new C&I solar (Ministry of New and Renewable Energy)

The direction is consistent across markets: decentralized, flexible, customer-side storage is now a policy priority.

4. Businesses want energy autonomy—not just lower bills

C&I customers are no longer thinking only in terms of cost savings. Their mindset has shifted toward resilience and control.

Top motivations reported in multiple markets include:

Protection against blackouts

Smoother energy supply for precision manufacturing

The technical ecosystem around C&I storage has become more standardized and robust in the last two years:

Liquid-cooled battery modules extend cycle life and improve safety

Modular PCS (50–125 kW) building blocks scale flexibly

All-in-one containers simplify installation and commissioning

Advanced BMS + EMS optimize both cost savings and battery health

10–20 ms STS modules deliver seamless backup switching

AI-driven scheduling boosts revenue in markets with time-of-use tariffs

This means businesses no longer need months of engineering and custom design; a 1 MWh system can be deployed like an appliance.

7. Why 500 kW–2 MWh specifically?

Because it fits the typical load profile of modern businesses:

A cold storage warehouse: 300–700 kW

A textiles or machinery plant: 500–1,200 kW

A logistics park: 300–900 kW

A shopping center: 400–800 kW

A single system in this size band allows customers to:

Reduce peak demand by 20–40%

Store 2–4 hours of backup energy

Integrate 500–1,500 kW of solar

Achieve ≤ 4-year ROI

Meet ESG or decarbonization commitments

Simply put: this size band perfectly aligns with the energy economics of the C&I sector.

Gogreen's real project of 500KW/860KWH Hybrid ESS in South African Logistic Park

🌱Gogreen Conclusion:

500kW/860kWh Hybrid ESSThe next wave of global energy transition is happening behind the meter

C&I energy storage is no longer an experimental technology or a niche solution. It is becoming a mainstream business asset, as fundamental as forklifts, servers, or backup generators.

The global shift from “grid dependence” to “energy autonomy” has begun—and the companies that adopt 500 kW–2 MWh systems today are positioning themselves at the forefront of this transformation.

As the world moves into 2025, one thing is clear: C&I storage is not just exploding—it's redefining how businesses think about power.